COVID-19 and Financial Markets: Part I

In this first article in a three-part series, Les Nemethy and Sergey Glekov use their regular Corporate Finance Column to look at the likely economic effects of the coronavirus.

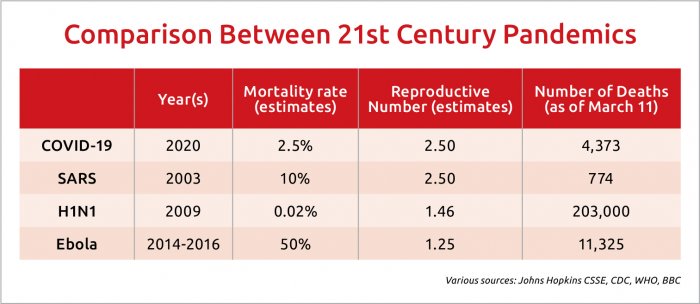

COVID-19 has taken approximately 4,370 lives to date, and infected approximately 121,570 people in more than 60 countries, according to Johns Hopkins Center for Systems Science and Engineering, as of March 11.

This article is not about the humanitarian aspects of COVID-19 (which are not to be underestimated); rather, we deal with three questions: as of today, knowing what one knows about the disease, can the disease be contained or will it become a pandemic; what effect can be expected on the economy and financial markets?; and what are the implications for personal investment decisions?

This first article deals with the first question only. We should emphasize that we are not medical experts, and have formed our worldview on this subject by an extensive literature review. It should also be emphasized that there is a great deal about COVID-19 that even the experts don’t know.

The virus has spread to all continents except for Antarctica. While the disease is believed to have originated in Wuhan, China, there are already more reported cases outside China than inside it.

The death rate of COVID-19 is estimated at between 0.5% to 4%, according to the opening remarks of World Health Organization Director-General Tedros Adhanom Ghebreyesus at a media briefing on February 24. The death rate may depend on factors such as quality of medical care, stage of disease at which the patient seeks medical care, age of patient, etc.

Another important indicator of any disease is its contagiousness or, in medical jargon, its “reproductive number”: the expected number of additional cases that one case will generate, on average, over the course of its infectious period.

From this point of view, COVID-19 is really more dangerous than seasonal flu, in that its reproductive number is 2.2, compared to 1.3 for most types of flu, according to the paper Early Transmission Dynamics in Wuhan, China, of Novel Coronavirus–Infected Pneumonia, published in the New England Journal of Medicine. In other words, not only is it deadlier than most types of flu (but not nearly as deadly as SARS), it is also more contagious—a kind of super flu.

COVID-19 has an incubation period estimated at 14 days, during much of which there are no symptoms, but the carrier of the virus is still contagious. This is possibly what makes containment of the virus so difficult. Newer ways of transmission are being discovered, via feces and through dogs, for example.

Rapid Spread

There are at least two types of environments in which the virus can spread more rapidly, and is likely to be more deadly:

• poor countries, characterized by lower quantity and quality of medical facilities and few resources; and

• authoritarian countries, where for political reasons, decision makers are in denial, or may constitute a bottleneck.

The first cases of COVID-19 have recently been reported in more crowded and less affluent countries such as India, Indonesia and Nigeria. Poorer countries like Niger and Togo have even poorer medical infrastructure. Countries like this are potential powder kegs. (Given that the virus spreads through feces, countries known for extensive outdoor defecation, like India, could be particularly vulnerable).

The degree to which the disease spreads in these poorer countries will be crucial to the global outcome. Even if developed countries with excellent containment programs, such as Singapore, are able to eradicate the disease, they may be faced with a difficult choice of cutting off travel from large swaths of the world, or will be under a threat of resurgence of the disease.

The big question is whether containment is still possible, or if COVID-19 will develop into a pandemic.

Given the covert ways in which the disease can be transmitted, and the large number of diagnosed cases, with many more cases possibly undiagnosed, it seems that we are well past the possibility of containment.

We see only three things that could eventually slow down the virus: Development of a vaccine (a possibility within 6-12 months); warming weather reducing transmission rates; and resistance levels building up in the human population (after large numbers of people have been exposed).

At some point, governments may decide that the effects of the cure are worse than the disease. If you lock down tens or hundreds of millions of people, and production stops, the economy collapses, and governments have a very different set of problems.

So, once the prevailing wisdom shifts to a view that containment has failed, we may see efforts to contain the disease called off or reduced, resulting in further contagion.

According to the WHO, seasonal influenza epidemics are estimated to result in about 3 million to 5 million cases of severe illness per annum, and about 290,000 to 650,000 respiratory deaths. COVID-19 may well just enter into the general influenza pool, albeit greatly augmenting the number of deaths, perhaps into the millions, at least for a few years.

(The world now experiences 1.35 million deaths from auto accidents a year, according to the Global status report on road safety 2018 by WHO. While the humanitarian cost is staggering, the world moves on.)

This is perhaps the most unfinancial article we have written. But the assumptions in this article will underpin our analysis in the next two articles, namely the effects on the economy and financial markets; and (implications for your investment portfolio.

Les Nemethy is CEO of Euro-Phoenix (www.europhoenix.com), a Central European corporate finance firm, author of Business Exit Planning (www.businessexitplanningbook.com) and a former president of the American Chamber of Commerce in Hungary.

Report Points to Increased Risk on Commercial Real Estate Ma...

Chinese President to Visit Budapest in May

Hungarian Gen Z Auto-buyers Prioritize Affordability

Liz & Chain Rooftop Bar Debuts Sustainable Cocktails

SUPPORT THE BUDAPEST BUSINESS JOURNAL

Producing journalism that is worthy of the name is a costly business. For 27 years, the publishers, editors and reporters of the Budapest Business Journal have striven to bring you business news that works, information that you can trust, that is factual, accurate and presented without fear or favor.

Newspaper organizations across the globe have struggled to find a business model that allows them to continue to excel, without compromising their ability to perform. Most recently, some have experimented with the idea of involving their most important stakeholders, their readers.

We would like to offer that same opportunity to our readers. We would like to invite you to help us deliver the quality business journalism you require. Hit our Support the BBJ button and you can choose the how much and how often you send us your contributions.