The Inflationary Impact on Developed and Emerging Markets

Les Nemethy and François Lesegretain investigate past and current differences in inflation rates between emerging markets (EMs) and developed markets (DMs) and the differences in performance among asset classes between EMs and DMs during periods of inflation.

During the past 25 years, inflation in EMs has been consistently higher than in DMs and much higher during two periods: 1994-2000 and 2018-2020.

U.S. inflation begun to outpace inflation across most DMs in 2021, reaching levels experienced in EMs, indicating an overheating of the U.S. economy, fuelled by monetary and fiscal stimulus.

Of course, if one looks at inflation on a country-by-country basis, results are more scattered, but the trend is upwards everywhere:

Inflation in emerging markets may have a much more disastrous impact than in developed markets. For example, the Arab Spring in 2011 was triggered by rapid inflation, particularly in the price of wheat.

Emerging markets equities are among the best performers in periods of high inflation and strong growth compared to other asset classes. For example, from 1987 to 2021, when global inflation was above 2%, EM equities were significant outperformers, generating average annual returns of almost 27%.

After a COVID-induced 2020 recession that was less severe in emerging markets than developed markets in terms of GDP impact, EM GDP growth is once again expected to outpace that of DMs, beginning with expectations for a robust recovery in 2021.

USD Debt

The outperformance of emerging market assets may also be explained by the fact that EMs do better in a time of a weakening U.S. dollar. This is because EMs tend to issue U.S. dollar-denominated debt; when the USD appreciates, the more local currency is required to service debt, putting a drag on the economy and increasing the probability of default.

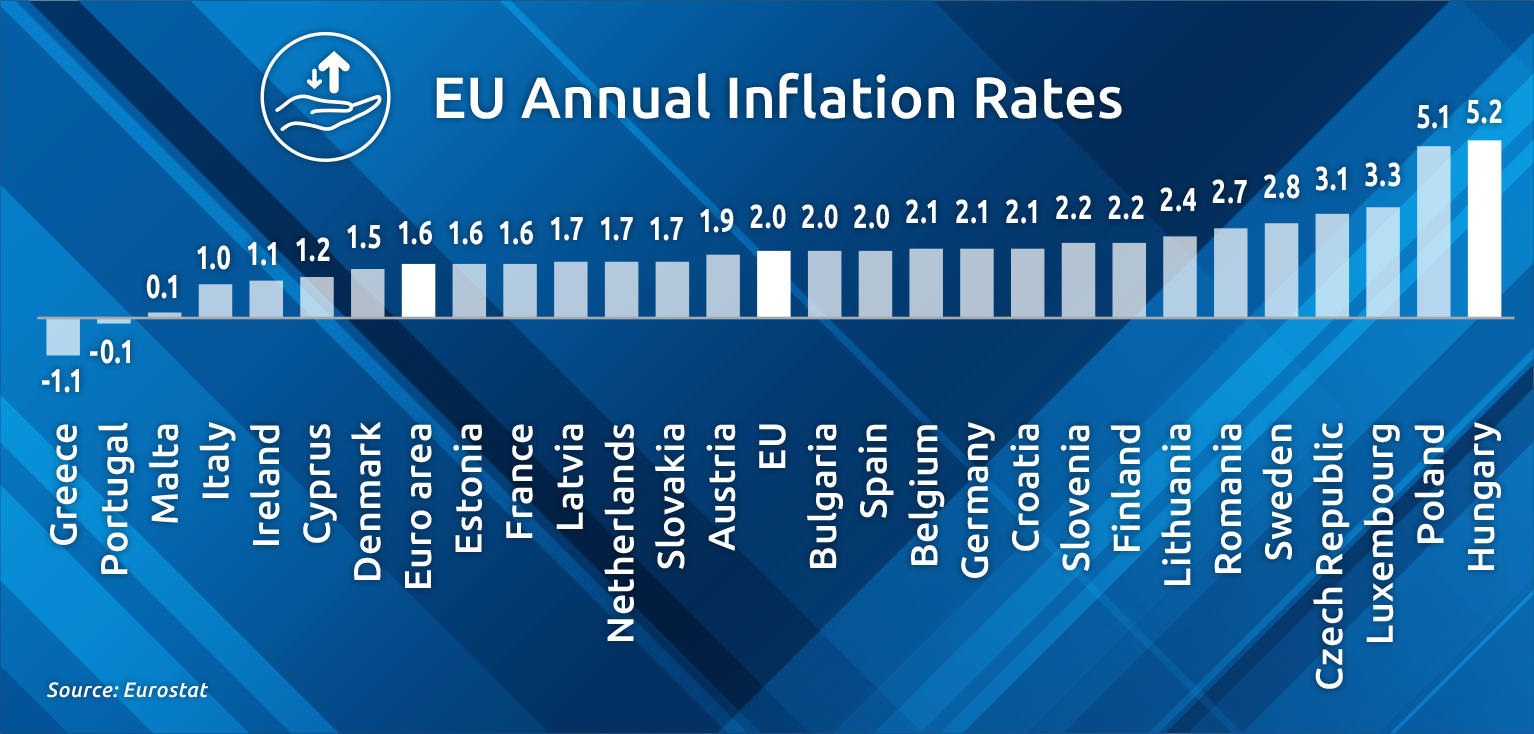

As of April 2021, Central European inflation rates are among the top in the European Union. Hungary, Poland, and the Czech Republic are experiencing inflation rates of 5.2%, 5.1%, and 3.1%, respectively.

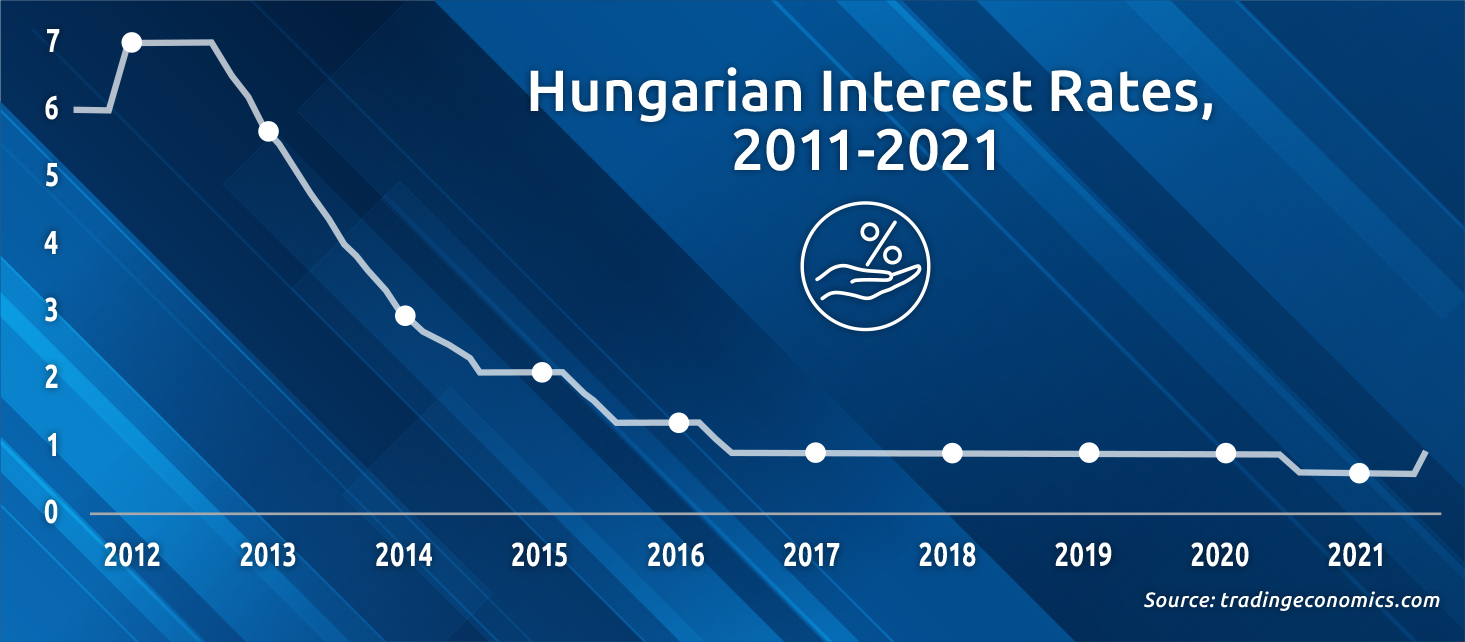

In Hungary, inflation recently reached an annual rate of 5.1%, above the central bank’s 3% headline inflation target. This is the country’s highest inflation rate since November 2012. Emerging markets do not have the luxury of allowing their economies and inflation rates to “run hot;” Brazil and Hungary have raised borrowing costs. The Monetary Council of the National Bank of Hungary (MNB), for example, increased the base rate by 30 basis points to 0.9% at a monthly policy meeting on June 22 of this year.

Similarly, the Czech central bank increased its key interest rate by a quarter-point to 0.5% in an effort to tame inflation as the economy recovers from the coronavirus pandemic.

Emerging markets have been a relatively better investment than developed markets over the years, whether you invested in equity or debt. But it is important to bear in mind that EMs will generally be subject to more significant political, legal, counterparty, and operational risks. Indeed, both returns and volatility in EMs have been relatively high over the past 20 years.

In terms of countries, the five best emerging market equity performers in 2020 were South Korea (44.64%), Taiwan (40.99%), China (29.49%), India (15.55%), and Argentina (12.7%).

It goes to show that investments in EMs have a place in any portfolio, particularly during a time of accelerating inflation. The choice of country, debt or equity, and the company issuing the debt or equity remain vital questions.

Les Nemethy is CEO of Euro-Phoenix Financial Advisers Ltd. (www.europhoenix.com), a Central European corporate finance firm. He is a former World Banker, author of Business Exit Planning (www.businessexitplanningbook.com) and a past president of the American Chamber of Commerce in Hungary.

This article was first published in the Budapest Business Journal print issue of July 2, 2021.

Hungary Gasoline Prices 3% Over Regional Avg

Hungary to Address Future of Cohesion Policy During EU Presi...

Cordia’s Marina City Project Begins

Budapest Airport Wins 'Best Airport in Eastern Europe' for 1...

SUPPORT THE BUDAPEST BUSINESS JOURNAL

Producing journalism that is worthy of the name is a costly business. For 27 years, the publishers, editors and reporters of the Budapest Business Journal have striven to bring you business news that works, information that you can trust, that is factual, accurate and presented without fear or favor.

Newspaper organizations across the globe have struggled to find a business model that allows them to continue to excel, without compromising their ability to perform. Most recently, some have experimented with the idea of involving their most important stakeholders, their readers.

We would like to offer that same opportunity to our readers. We would like to invite you to help us deliver the quality business journalism you require. Hit our Support the BBJ button and you can choose the how much and how often you send us your contributions.