Skyrocketing Industrial Output Promises Higher Annual Growth

Although credit rating agency Moody’s chose not to update Hungary’s sovereign rating at its scheduled review at the beginning of May, the country did receive an optimistic prognosis from the European Commission. The latest industrial output data seems to justify increased expectations for this year’s GDP growth.

There is no logical explanation why Moody’s Investors Service missed reviewing Hungary’s sovereign rating, although it was scheduled for May 3, analysts said after the agency did not issue an update on the country’s rating.

At the previous review, on November 23, 2018, Moody’s left the rating unchanged at Baa3, one notch above the investment grade threshold, with a stable outlook. S&P Global Ratings and Fitch both upgraded Hungary to ‘BBB’, two notches above the investment grade threshold, in February of this year.

Not completing the scheduled review was absolutely groundless, said Gergely Suppan, head analyst at Takarékbank. He added that credit rating agencies are lagging behind Hungary’s economic progress.

“The Hungarian economy expands dynamically and sustainably, and also in a balanced way, external debt ratio sharply falls due to the strong external financing abilities, and the government debt will also decrease substantially and it could fall below 60% of the GDP within two years,” Suppan emphasized.

The generally deteriorating external environment could explain the cautious approach of Moody’s, but Zoltán Török, head analyst at Raiffeisen Bank, believes there is still a good chance that Moody’s will upgrade the country soon, to bring it back in line with the other two international credit rating institutions. The balanced economic growth, the status of the current account and the relatively low inflation all support a positive decision in the future, he added.

Unexplainable

Török also said that no significant changes are expected in the above mentioned positive economic data, even in the midst of deteriorating external circumstances. These factors were enough for Standard & Poor’s and Fitch to upgrade Hungary’s sovereign rating in February, which makes the Moody’s decision even more surprising and unexplainable.

Gábor Regős, head of the macroeconomics division of economic research institution Századvég Gazdaságkutató was equally unable to explain why Moody’s did not review Hungary’s debt rating on May 3. He mentioned the dynamic GDP growth, the decreasing state debt ratio, and also the increasingly safe financing of the state debt as positive factors. He also emphasized that the markets now trust in the Hungarian economy, which is clearly shown in yield levels.

While most analysts were taken by surprise by Moody’s move, or perhaps more accurately lack of a move, K&H Bank analyst Dávid Németh voiced a different opinion.

“One couldn’t have expected an upgrade by Moody’s,” the analyst told a television program on the day after. According to him, Moody’s cited several risk factors in its latest review last fall, and as it hasn’t received reassuring data regarding such risks, it was not surprising that it had not issued an update. The risks Moody’s listed includes the overheated labor market and the impact of the slowing automotive sector in Europe.

However, just a few days after the disappointing non-news from Moody’s, another positive opinion was issued regarding Hungary’s growth potential. The European Commission raised its projection for Hungary’s GDP growth this year to 3.7% from 3.4% in a quarterly forecast released on May 7. It also raised the forecast for next year’s growth to 2.8% from 2.6%.

The Commission noted that low unemployment and continued minimum wage rises are projected to keep wage increases above productivity growth. It added that households are expected to spend an increasing share of their income on housing due to rising home prices and expanded government support targeting first-time home buyers.

Balanced Risks

The EC did warn that there are some risks to the forecast as well, but says these are balanced, with external risks on the downside and domestic risks on the upside as the tight labor market could sustain even higher wage and consumption growth.

Consumer price inflation is set to rise to 3.2% in both 2019 and 2020, driven by rapid growth of unit labor costs and consumption. The EC sees the general government deficit narrowing to 1.8% of GDP in 2019 and 1.6% in 2020, but said that a more rapid growth of public investment and a potentially higher take-up of government measures that aim to boost the birth rate do pose risks.

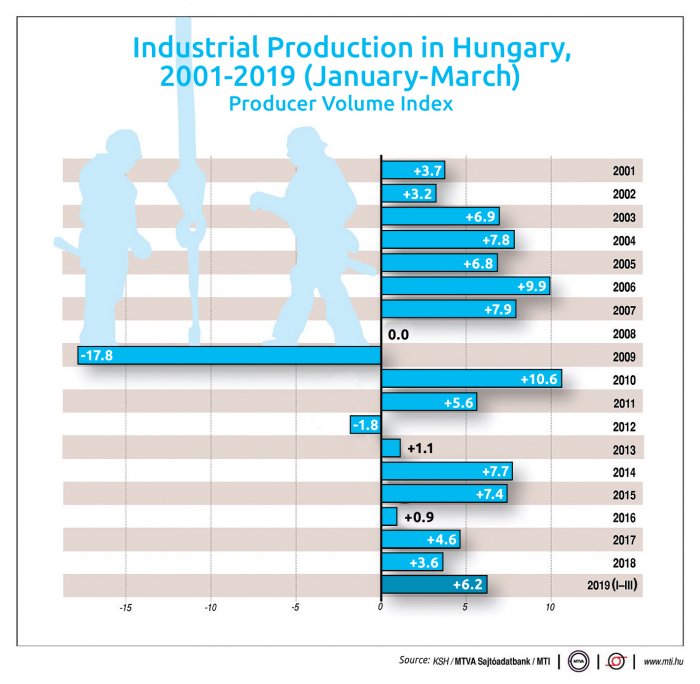

Hungary‘s updated Convergence Program, which was presented to the European Commission in early May, puts GDP growth in both years at 4%. Such expectations might be well-grounded, especially in the light of the latest industrial data: in March 2019, the volume of industrial output – both in raw terms and according to working day-adjusted figures – grew by 8% year-on-year, according to a first reading of data from the Central Statistical Office (KSH).

Suppan said in a note that Takarékbank could now modify upward its annual GDP forecast of 4.4%. Other analysts followed suit: Orsolya Nyeste of Erste Bank emphasized that Hungarian industry had proved to be resistant to international shocks, and she now expects strong GDP growth for the first quarter of 2019, at around 5%. Németh of K&H Bank thinks that the annual growth rate of Hungary’s industrial output might reach 5% this year.

MOL Shareholders Approve Dividend of Around HUF 250/Share

Gov't Awards HUF 6.5 bln of Subsidies to SMEs in Underdevelo...

Hungary's Largest ESG Consultancy Formed by Merger of EY, De...

Liz & Chain Rooftop Bar Debuts Sustainable Cocktails

SUPPORT THE BUDAPEST BUSINESS JOURNAL

Producing journalism that is worthy of the name is a costly business. For 27 years, the publishers, editors and reporters of the Budapest Business Journal have striven to bring you business news that works, information that you can trust, that is factual, accurate and presented without fear or favor.

Newspaper organizations across the globe have struggled to find a business model that allows them to continue to excel, without compromising their ability to perform. Most recently, some have experimented with the idea of involving their most important stakeholders, their readers.

We would like to offer that same opportunity to our readers. We would like to invite you to help us deliver the quality business journalism you require. Hit our Support the BBJ button and you can choose the how much and how often you send us your contributions.