Corporate Debt in Central Europe

Non-financial corporations can typically use two types of debt funding – bank loans and debt securities (e.g. bonds). Choosing one of them, or the right mix, depends on a company’s maturity, the industry and its cyclicality, interest rates, and other factors, Les Nemethy and Sergey Glekov argue in their latest column.

By way of example, during the financial crisis of 2008-09, non-financial corporations in the eurozone reacted to tightening bank lending conditions by shifting their debt composition from bank loans towards debt securities.

At the same time, the cost of market debt rose together with and exceeded the cost of bank debt, as pointed out by Fiorella De Fiore and Harald Uhlig in “Corporate Debt Structure and the Financial Crisis”.

The corporate debt ratio in the euro area increased considerably over the last 15 years, rising to 109% of the euro area’s gross domestic product by Q2 2019, but down from a peak of 115% in the first quarter of 2015.

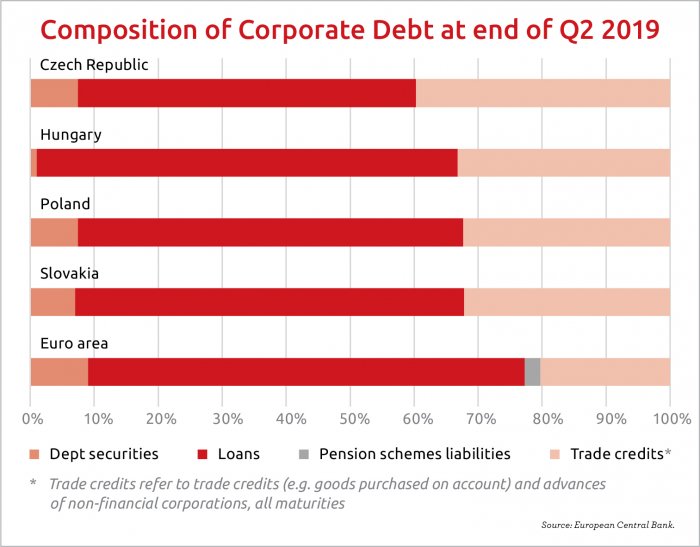

Total indebtedness of non-financial companies in the less developed countries of the EU is considerably lower: the corporate debt ratio in the Visegrád countries (the Czech Republic, Hungary, Poland and Slovakia) varies between 44% to 66% as of Q2 2019.

Although the composition of corporate debt varies among countries, bank loans are by far the more widely used instrument. On average, 68% of total euro area corporate debt consists of bank loans.

Loans Dominate

In the Visegrád Four countries, loans dominate the composition of corporate debt to an even greater degree: debt securities (corporate bonds) have a relatively low share (9%) in the debt structure within the euro area (with an exclusion of France). In the Visegrád Four countries, the share of debt securities is even below 9% of total corporate debt.

Indeed, in Hungary, debt securities account for only 1% of total corporate debt, the second lowest in the EU, ranking only slightly higher than Romania. One can only speculate that this might be due to a highly developed banking sector, and perhaps a dearth of potential Hungarian issuers.

There is a positive correlation between economic development and levels of outstanding bonds of nonfinancial corporations, as a percentage of GDP; in the more developed countries of the European Union, not only the total indebtedness of the companies, but also the volume of their funds raised on the bond market substantially exceeds that observed in the less developed countries.

A robust corporate bond market can act as a source of stability, especially in periods of financial instability, when the freezing up of bank credit is common. Moreover, the corporate bond market can create competition for bank loans, pushing the cost of borrowing for non-financial corporations lower and forming more attractive funding options.

In Hungary, debt financing is especially focused on the banking sector. Over time, it may be expected that Hungary will tend to converge towards European trends, with more financing to come from the corporate bond market.

Liquidity Injection

In order to increase the liquidity of the corporate bond market, the National Bank of Hungary (Magyar Nemzeti Bank, or MNB for short) launched its Bond Funding for Growth Scheme (BGS) on July 1.

The MNB has committed a facility of HUF 300 billion (approximately EUR 90 million) whereby the central bank will purchase bonds with at least “B+” ratings issued by domestic non-financial corporations as well as securities backed by corporate loans.

On October 24, alternative energy company Alteo, to quote just one example, raised almost HUF 9 billion from the sale of corporate bonds issued under this program, according to portfolio.hu in its article “Közel 9 milliárd forintos kötvénykibocsátás az Alteonál” (“Alteo issues bonds of nearly HUF 9 bln”).

Bank interest rates for loans to corporations with an original maturity of more than two years are lowest in Hungary and Slovakia. The latter is the only member of the V4 that is also simultaneously a member of the eurozone.

Slovakian interest rates have been consistently lower than those of other Visegrád countries. This may be attributed to Slovakia belonging to the eurozone: a serious competitive advantage for Slovak corporations. It goes to show that Hungary, Poland and the Czech Republic joining the eurozone could also serve to increase the competitiveness of corporations in those countries.

Les Nemethy is CEO of Euro-Phoenix (www.europhoenix.com), a Central European corporate finance firm, author of Business Exit Planning (www.businessexitplanningbook.com) and a former president of the American Chamber of Commerce in Hungary.

ÁKK Sells HUF 50 bln of Bonds at Auction, Over Plan

Hungary to Address Future of Cohesion Policy During EU Presi...

SUPPORT THE BUDAPEST BUSINESS JOURNAL

Producing journalism that is worthy of the name is a costly business. For 27 years, the publishers, editors and reporters of the Budapest Business Journal have striven to bring you business news that works, information that you can trust, that is factual, accurate and presented without fear or favor.

Newspaper organizations across the globe have struggled to find a business model that allows them to continue to excel, without compromising their ability to perform. Most recently, some have experimented with the idea of involving their most important stakeholders, their readers.

We would like to offer that same opportunity to our readers. We would like to invite you to help us deliver the quality business journalism you require. Hit our Support the BBJ button and you can choose the how much and how often you send us your contributions.