Asset Classes: Bonds

In their latest in a series of articles on various asset classes, Les Nemethy and Sergey Glekov turn their attention to bonds.

We often hear comments about how little interest banks pay, or the low yield on certain treasuries. In our business of Mergers & Acquisitions, we have seen quite a few business owners who want to sell their businesses, but hesitate to do so, because they do not know how to generate a decent return on their proceeds.

The good news is that through a diversified medium-risk bond portfolio, it should be possible to generate a return of 6-8% per annum. Rather than you working, let your money work for you!

Part I of this series provided an overview of asset classes; Part II dealt with the size and liquidity of the various public markets in which these asset classes trade. This article zeroes in on bonds, one of the most important asset classes.

On the U.S. bond market, Treasury Securities (a government debt instrument issued by the United States Department of the Treasury) and Corporate Bonds account for 57% of the whole market, with mortgage related securities, municipal bonds, and other more exotic bonds accounting for the balance. Hence, we will focus on treasuries and corporates for the remainder of this article.

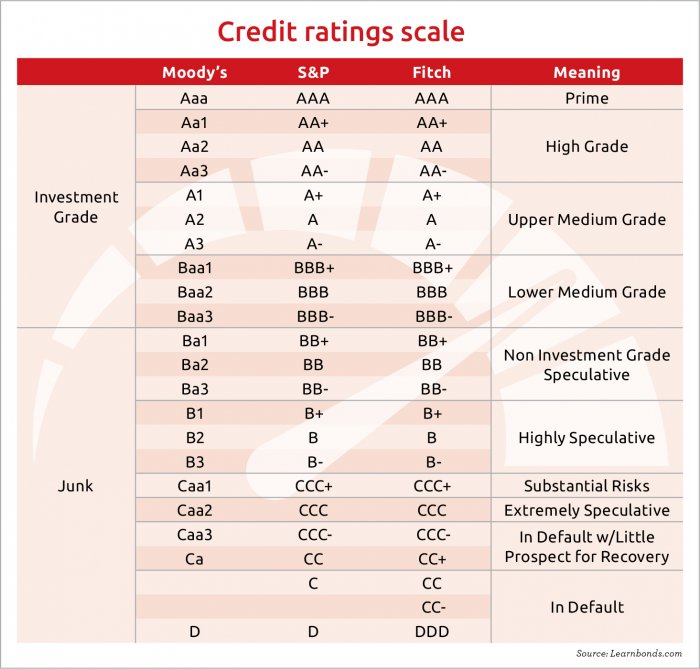

A useful tool for determining the likelihood of government or corporate default is a credit rating. The three major rating agencies are Moody’s, Standard and Poor’s, and Fitch:

Each investor who decides to invest in bonds as an asset class should construct his or her own bond portfolio, with the appropriate degree of risk/return relationship. (Usually this would be in conjunction with investing in other asset classes as well.)

The next chart provides a sample of various maturities of corporate bonds, to illustrate available of risk/return relationships.

So how often do bonds default? According to S&P’s 2017 Annual Global Corporate Default Study, higher grade and shorter-term bonds default quite seldom. Only 2% of investment grade bonds (e.g. credit rating of Baa3/BBB- and higher) are expected to default under a ten year time horizon.

Yields, meanwhile fluctuate over time. Since the end of the last financial crises, yields on Aaa bonds have fluctuated between 3-5% and Baa bonds between 4-7%. We are not suggesting an investment in bonds is for everyone. For example, it takes a fair amount of resources to build a balanced portfolio when bonds are typically sold in denominations of USD 100,000. However, we trust we have illustrated the principle that a 6-7% overall yield even in today’s low yield market should be achievable with relatively modest risk, and that bonds of various types should be seriously considered by most investors.

Disclaimer: This article is intended for informational purposes only, and should not be relied upon for investment advice. It is important to do your own investigation and analysis before making any investments based on your own personal circumstances.

Les Nemethy is CEO of Euro-Phoenix (www.europhoenix.com), a Central European corporate finance firm, author of Business Exit Planning (www.businessexitplanningbook.com) and a former president of the American Chamber of Commerce in Hungary.

Hungary Gasoline Prices 3% Over Regional Avg

Hungary to Address Future of Cohesion Policy During EU Presi...

Cordia’s Marina City Project Begins

Budapest Airport Wins 'Best Airport in Eastern Europe' for 1...

SUPPORT THE BUDAPEST BUSINESS JOURNAL

Producing journalism that is worthy of the name is a costly business. For 27 years, the publishers, editors and reporters of the Budapest Business Journal have striven to bring you business news that works, information that you can trust, that is factual, accurate and presented without fear or favor.

Newspaper organizations across the globe have struggled to find a business model that allows them to continue to excel, without compromising their ability to perform. Most recently, some have experimented with the idea of involving their most important stakeholders, their readers.

We would like to offer that same opportunity to our readers. We would like to invite you to help us deliver the quality business journalism you require. Hit our Support the BBJ button and you can choose the how much and how often you send us your contributions.